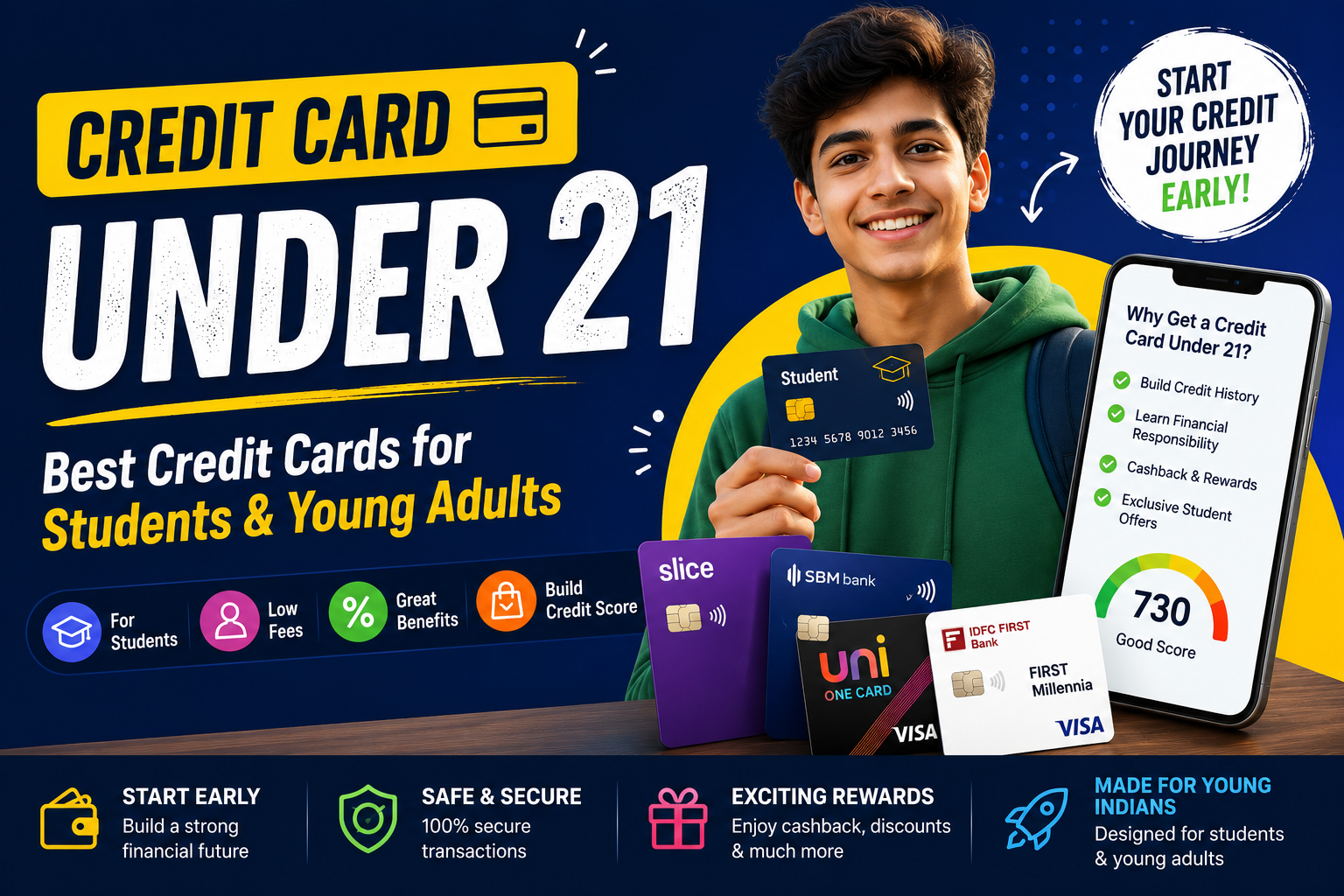

Start your credit journey early looks great on a carousel ad. Your future self cares less about the carousel and more about whether you missed a due date during exam week. In India, getting a credit card before 21 is possible — but the honest answer splits into three lanes: what law and RBI norms allow, what each issuer’s age rule prints on the application form, and whether you have income visibility, family support, or collateral the bank can lean on.

Below is the under-21 playbook for 2026: why many mainstream cards quietly say 21+, which routes actually work at 18–20, and a shortlist of real products on CardCheck so you compare fees and rewards instead of trusting a random infographic.

Cards in this comparison

Compare nowIndia under 21: hype vs underwriting

People love a clean story: everyone deserves credit at eighteen. Banks love a clean risk file: stable income, address proof, and a repayment track record they can model.

The gap between those two sentences is where young applicants live. Nobody is owed approval — but if you pick the right lane (add-on, secured, or a starter product with realistic published floors), you are not guessing in the dark.

Age 18 vs 21 — why the internet argues about it

You can legally enter many credit relationships as an adult at 18. Several issuers publish minimum age 18 on entry products. A different set of mainstream unsecured cards list minimum age 21 alongside ₹15,000–₹25,000/month style income floors.

So “can you get a card under 21?” is technically yes, and “can you get every popular cashback card under 21?” is often not without meeting that card’s exact rules — or using a family add-on.

Practical cheat sheet

| Situation | Typical path | Reality check |

|---|---|---|

| Under issuer’s primary age | Add-on card on parent’s account | Spend appears on the primary’s statement; learn limits before you flex on group orders. |

| 18+ but thin income proof | FD-backed / secured card | Limit tracks collateral; still need discipline on full payment. |

| 18+ with modest documented income | Entry unsecured with published min income + CIBIL | Compare our data to the live form — promos and rules move. |

| 21+ & working / interning | Lifetime-free digital cards | More options open; rewards maths still has caps and MCC quirks. |

Four routes that actually show up in real applications

1) Supplementary (add-on) card — Often the first “real” card for college: limit is shared with the primary, controls vary by issuer, and KYC rides on the parent’s relationship with the bank.

2) Fixed-deposit secured cards — Approval leans on money locked with the bank, not a salary slip narrative. Great when you can park cash without needing it for emergencies next week.

3) Published “starter” unsecured cards — Small annual fees or lifetime-free products with explicit CIBIL and income floors in disclosures. If you meet them on paper, you can still be declined for internal policy — that is normal, not a personal conspiracy.

4) Student-positioning products — Some banks market student journeys; eligibility is still bank-specific. Use the issuer’s page for documents, not a tweet thread.

Cards to compare on CardCheck (under-21 friendly angles)

These are catalog-backed picks with different “how you qualify” stories. Open each page for full benefit lines, exclusions, and APR bands — the lines below are a map, not a substitute for MITC.

OneCard Metal Credit Card

Why it fits the vibe: Published minimum age 18 in our data, lifetime free, ₹20,000/month minimum income, 650+ CIBIL, 5X points on top two spend categories each month (auto-tracked), 1X elsewhere, 0% forex markup.

Witty but true: the app thinks it is your strategist. You still have to be the adult who pays the full statement.

IDFC FIRST WOW! Credit Card

Why it fits the vibe: FD-backed path in our positioning; ages 18–70; lifetime free in captured fee fields; 0% forex markup; no minimum income / CIBIL floor in the catalog for this product — the FD is the point.

ICICI Bank Platinum Chip Credit Card

Why it fits the vibe: Minimum age 18, ₹0 joining and annual fee, ₹15,000/month income and 650+ CIBIL in our data — a plain vanilla on-ramp if you want simple points without metal flex.

IDFC FIRST Millennia Credit Card

Why it fits the “almost 21 / already earning” reader: Lifetime free, strong online multipliers on select merchants, but published minimum age 21 and ₹25,000/month / 700+ CIBIL in our snapshot — bookmark it for the birthday after you have income proof.

SBI Unnati Credit Card

Why it fits the vibe: Secured against SBI fixed deposit (we capture ₹25,000 minimum deposit), 1% cashback on eligible retail in our lines, minimum age 18, ₹499 annual fee in captured data — issuer copy in our database also notes a first-four-years fee waiver pattern when there is no default; confirm the live MITC.

Credit history without theatre

- Pay full, not WhatsApp-reminder roulette. Interest and late fees erase snack-level cashback gains fast.

- Keep utilization sane on low limits — maxing a ₹20k line every month “for points” is how profiles look stressed.

- One card done well beats four cards you forget to lock when the phone is stolen.

When you are ready to graduate from “will I get approved?” to “which card pays for my actual life?”, run the Rewards calculator on real rupee spends and the card quiz for a short shortlist.

When to wait — and when to apply

Wait if you do not have a repayment plan (part-time gig income is fine if it is predictable enough for you — banks still underwrite unpredictably).

Apply when you understand annual fee, APR if you rotate balances, and the documents each issuer lists today.

If you want blunt, low-stakes commentary after you choose, Card roast is there — vibes only, not financial advice.

FAQ

- Can you get a credit card under 21 in India?

Often yes, but not on every product. Paths that work before 21 include add-on cards, FD-backed secured cards (like IDFC FIRST WOW! in our data), and some starter unsecured cards with minimum age 18 (for example ICICI Platinum Chip). Many mainstream picks still say minimum age 21 — check the exact rule on each card page.

- What is the minimum age for credit card in India?

Issuers publish different minimum ages — commonly 18 on some entry routes and 21 on several unsecured mass-market cards. Parents and bankers both agree only on one thing: the number on your PAN matters less than matching the issuer’s published minimum for that product.

- Is a student credit card different from a normal credit card?

Marketing labels vary. Whatever it is called, read fees, credit limit, reward exclusions, and documents like a normal card. On CardCheck, compare IDFC WOW versus OneCard Metal and see which underwriting story matches your situation.

- Best credit card for 18-year-old in India with no salary proof?

The dependable answers are add-on, secured / FD-backed (IDFC WOW or SBI Unnati in our catalog positioning), or any route your bank documents without traditional salary slips. Approval is never guaranteed.

- Do I need a CIBIL score under 21?

Some products list a minimum CIBIL; secured paths may be more forgiving because risk is collateral-backed. Thin files exist — banks still decide case by case.

- Does CardCheck approve applications?

No. We compare issuer-sourced disclosures side by side so you prepare better answers and fewer surprises.