You already speak fluent UPI: tap, OTP, done. A credit card is the same plastic reflex with a different boss — you are spending the bank’s money first, under rules India’s banking regulator (the Reserve Bank of India) expects issuers to disclose.

The bank gives you a limit, you spend, you get a statement with a due date. Pay in full and on time, and the product is mostly discipline plus perks. Treat the limit like a personality buff, and the statement will humble you faster than a cousins’ group chat.

This is a Gen Z–friendly beginner map: what a card is, how billing works, what CIBIL is actually about, where fees hide, how RuPay fits your UPI habits, and a few starter picks to compare on CardCheck — always confirm fees and eligibility on the issuer’s MITC (the bill-terms PDF), not from a random infographic.

Cards in this comparison

Compare nowWhat a credit card is (and what it is not)

A credit card is a line of credit: spend up to a credit limit, repay per the issuer’s Most Important Terms and Conditions.

What it is not: extra salary, a loyalty programme with cinematic lighting, or “free money until the algorithm likes you again.”

| Debit | Credit | |

|---|---|---|

| Whose cash | Money already in your account | The bank’s until you repay |

| Interest story | Not the same revolving-balance drama | Very expensive if you roll balances — read MITC |

| Why people bother | Simplicity | Rewards, purchase protections where applicable, credit history |

How it works: billing, due dates, and the grace period

The three dates that matter

Statement date: the bank closes the tab and generates the bill. Due date: when you should clear what you owe to stay clean. Grace period: the window where full payment on purchases can avoid interest — if your issuer’s rules say so. Never assume; read the product terms.

Full payment vs minimum due

Paying in full is the boring flex that keeps finance Twitter from ratio-ing you. Paying only the minimum due is how a small balance becomes a long season of interest — revolving APRs in India are typically very high versus almost anything else you would voluntarily carry long term. Want a number? Open your issuer’s MITC like someone who enjoys sleeping.

Credit score explained (without astrology)

People say CIBIL the way they say “Wi-Fi password” — casually, but it gates real doors. Lenders look at repayment behaviour, utilisation, enquiries, and more; exact weighting is not a public cheat code.

Beginner moves that age well:

- Pay on time, ideally full.

- Avoid spraying five applications in one emotional evening — hard enquiries leave footprints.

- Keep utilisation sane. Maxing a tiny limit every month “for points” is stress wearing a trench coat.

Fees and fine print your thumb usually scrolls past

Annual / joining fee: sometimes ₹0, sometimes not — waiver rules often depend on spend targets. If you will not hit the target, do not cosplay someone who will.

Forex markup: international spends can stack extra cost layers — compare cards here, then verify on the bank site.

Cash advance: withdrawing cash on a card is how you invite fees plus interest to the party early.

Rewards fine print: caps, excluded merchant categories, and “accelerated” categories that mainly accelerate marketing metrics.

RuPay, Visa, Mastercard — and why UPI habits still matter

You might live on UPI. Credit cards still matter because they build repayment history and can bundle structured benefits when you stay inside the rules.

RuPay credit cards are part of India’s stack; acceptance and merchant setup evolve — if a weekend plan depends on a network, sanity-check it before you bet the group order on vibes alone.

Starter picks to compare (not approval promises)

Nobody serious guarantees approval. These are common first-card lanes to explore on CardCheck, then verify on the issuer application page.

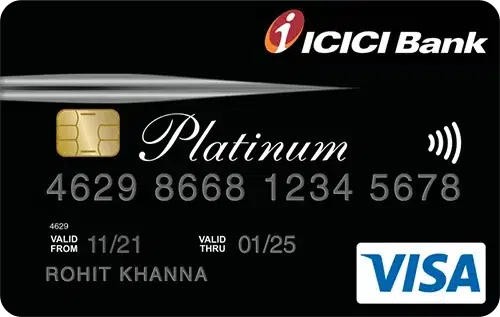

ICICI Bank Platinum Chip Credit Card

Who it suits: readers who want a simple entry with a low-fee-shaped story in many portfolios — still subject to underwriting.

Kotak 811 Dream Different Credit Card

Who it suits: people already inside 811-style digital banking — convenience only helps if you still respect the due date.

Flipkart Axis Bank Credit Card

Who it suits: heavy online shopping spenders who will actually use the category story.

Axis Bank ACE Credit Card

Who it suits: cashback-focused users who are fine with fee plus rules complexity — read caps like patch notes.

IDFC FIRST WOW! Credit Card

Who it suits: if unsecured approval is uncertain, FD-backed routes can be a regulated on-ramp — cash is still locked; it is not “no money,” it is “money on pause.”

Seven beginner mistakes that are not cute

- Treating credit limit like income

- Subscriptions stacking until your statement looks like a festival lineup

- Assuming minimum due is “smart” because the app allows it

- Chasing metal before you can pay full

- Applying everywhere after one rejection

- Using cash advance because “liquidity” sounds clever

- Ignoring SMS alerts until the bank becomes your most consistent relationship

Your first 30 days with a card (checklist)

- Set autopay for full if cash flow supports it.

- Turn on transaction alerts.

- Read MITC for interest, forex, and fee triggers — yes, it is long; so is regret.

- Pick one primary spending card for the first quarter — complexity is not a personality.

- After a few cycles, pull your credit report and see what is reporting.

When you are ready to match a card to your rupee life, use CardCheck’s free Quiz — about one minute — then confirm everything on the issuer site.

FAQ

- Is a credit card “safer” than UPI?

“Safer” depends on fraud type and issuer protections. What is objectively true: a card is credit with repayment rules — treat disputes and locks as a process, not a vibe.

- Will I get approved as a student or fresher?

Sometimes via secured products, add-on cards, or issuer-specific programmes. Nobody reputable guarantees approval — use tools here, then read the bank’s eligibility copy.

- Should I get two cards immediately for utilisation optimisation?

Master one bill first. Two cards means two due-date personalities — you are still one human.

- Does browsing CardCheck hurt CIBIL?

Reading comparison pages does not magically hit your bureau. Applications trigger lender checks — those matter.

- Does CardCheck approve applications?

No. We line up issuer-sourced disclosures so you prepare fewer surprises.