You will not usually see “This card needs CIBIL 742” on a bank’s public page. Approval looks at your CIBIL / bureau score plus income, job, banking history, limits you already have, and your full credit report — not only one number.

Below: what TransUnion CIBIL itself says (with a link), why MITC booklets do not list a score per card, a simple band table for learning only — not a promise from any issuer — and RBI for your rights on credit information.

Cards in this comparison

Compare now

What the CIBIL score is (in short)

TransUnion CIBIL calls it a 3‑digit summary of how you repaid past loans and cards, built from your credit report (read on CIBIL).

They state scores range from 300 to 900; higher is better for approval odds. In the same article they note that 79% of loans go to people with a score above 750 — a wide market picture, not your personal guarantee. Cards use the same bureau habit; each bank still sets its own rules.

They highlight four areas that matter: payments on time, mix of secured vs unsecured loans, not too many loan applications at once, and not maxing out cards every month.

Why there is no printed “780 for this card”

Your MITC booklet is about fees, interest, and billing — not a fixed CIBIL number for each product name. Banks change internal rules; the same card online vs branch can even differ.

What you will see: eligibility blurbs (age, income), FD‑backed cards for first‑time borrowers, and ads for “pre‑approved” offers — always read the small print (income and other checks still apply). For what RBI says about credit reports, see these FAQs.

In practice (plain English, not a law)

In real life, banks like to see a healthy score — often 750+ feels “comfortable” for many unsecured products, but many people in the 700–750 range still get cards when salary, report, and enquiries look fine. Below ~650–700 gets harder for standard cards unless other factors (relationship, secured product) help.

So: one number is never the whole story. Income, EMI burden, recent applications, and mistakes on the report matter just as much.

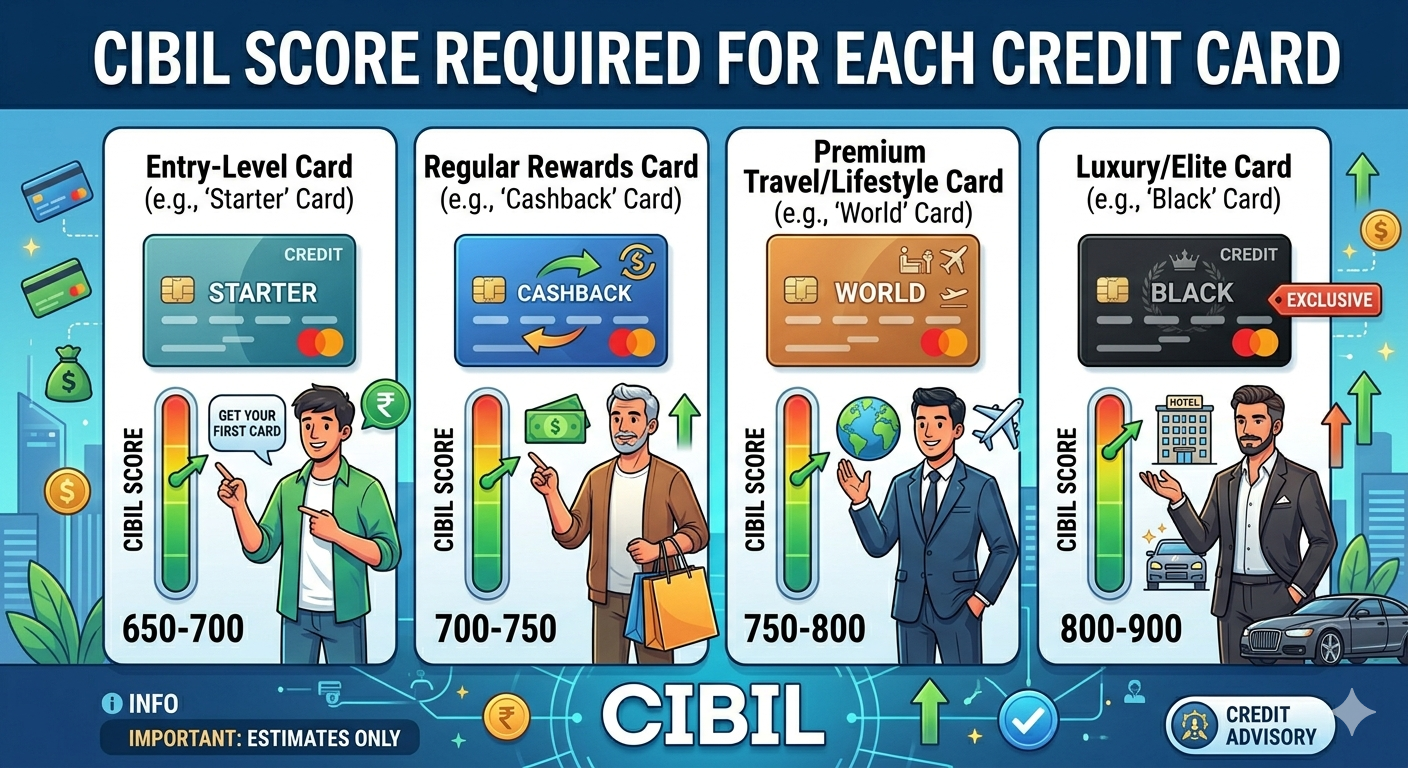

Illustrative bands (learning only)

Use this only to get a feel. It does not replace a bank’s yes or no.

| Card type (rough) | Rough CIBIL band | What it usually means |

|---|---|---|

| Starter / first card, thin file | 650–700 | Tougher for normal cards; FD / secured routes are common on issuer sites. |

| Everyday cashback / basic rewards | 700–750 | Often workable if income and payment history look clean. |

| Mid / travel rewards | 750–800 | Aligns with where CIBIL’s own data shows heavy approval share above 750 — still need income fits. |

| Top / invite-style lines | 800–900 | Strong record helps; salary caps and bank rules still decide. |

Example cards on CardCheck (not score promises)

Examples from entry to premium — we only show product kind, not “your score must be X”. Compare cards shows fees and rewards from issuer data.

- Amazon Pay ICICI Credit Card — wide cashback entry.

- SBI SimplyCLICK Credit Card — everyday online rewards.

- HDFC Regalia Gold Credit Card — mid travel / lounge segment.

- Axis Magnus Credit Card — premium perks.

Disclaimer

General education. Numbers 300–900, 79%, and above‑750 wording come from TransUnion CIBIL’s consumer article (link).

Your issuer, income, existing debt, and fresh report beat any article. Read MITC for rates and fees.

FAQ

- Did RBI fix one minimum CIBIL for every card?

No. RBI oversees banks and bureaus; each bank sets approval rules. RBI FAQs explain your rights about credit data — not a score table per card.

- Which one figure should I remember?

Scale: 300–900. Higher is better. CIBIL’s article links strong approvals in bulk data to > 750 — that is not a promise for you personally.

- If my score is high, will the bank skip income checks?

Usually no. High EMIs vs salary, many new applications, or thin history can still trigger a no.

- Should I chase the fanciest “tier 4” card?

Only if annual fee, interest, reward caps, and your spend justify it. Comfort matters more than status.