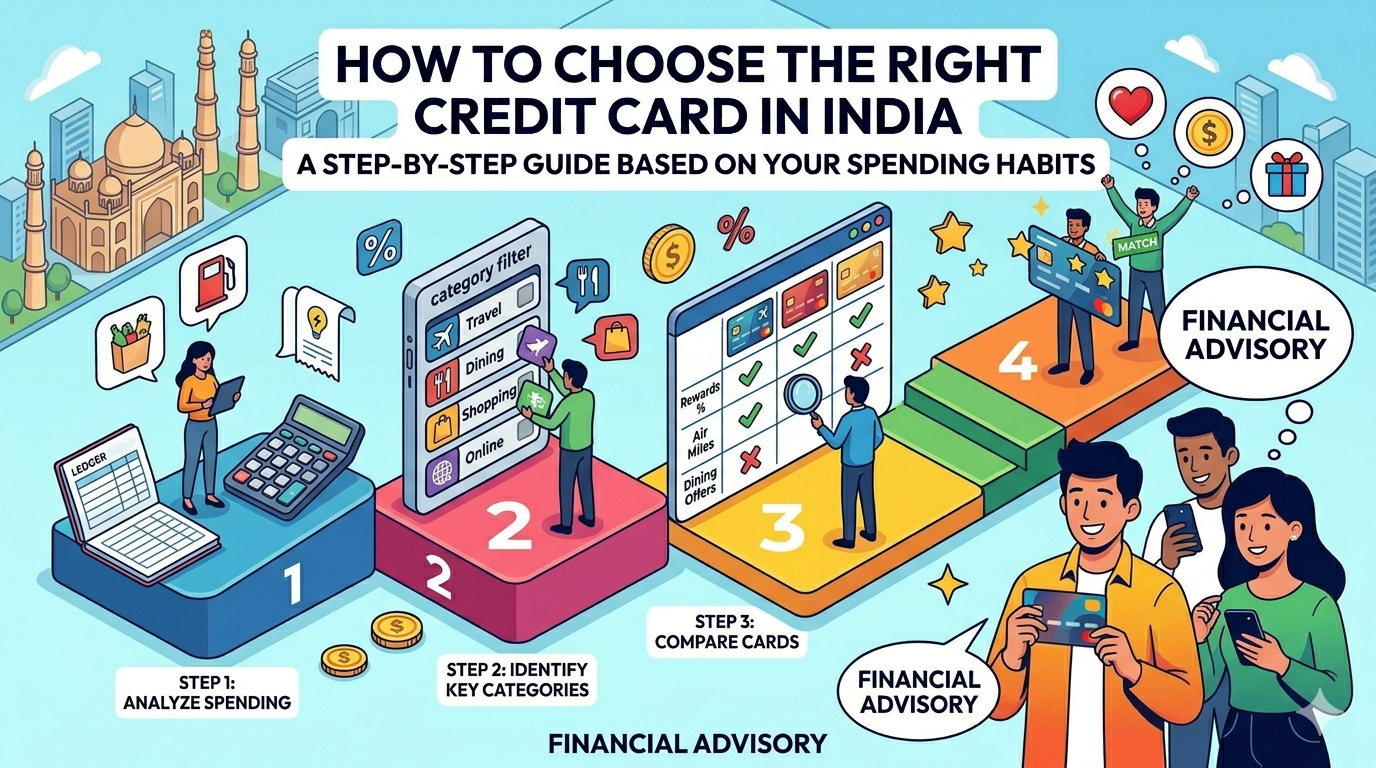

Brochure या 'pre-approved' SMS से credit card चुनना fast है। लेकिन एक card जो आपके actual spending के साथ match करे, उसके लिए एक structured pass चाहिए — और यह आमतौर पर पहले साल में ही return देता है।

यह guide आठ practical steps से गुज़रती है: spend quantify करना, credit use decide करना, categories match करना, fees और caps check करना।

Cards in this comparison

Compare now

Step 1 — लिखें कि आपका पैसा कहां जाता है

पिछले 2–3 महीनों के spends देखें (bank statement, credit card statement, या UPI history)। Roughly bucket करें:

- Online retail (Amazon, Flipkart, brand sites)

- Food delivery और dining

- Groceries और supermarkets

- Fuel

- Bills और utilities (electricity, broadband, mobile)

- Travel (flights, hotels, train)

- अन्य

Step 2 — Honest रहें: क्या आप हर महीना full statement भरेंगे?

अगर हां (transactor): earn rate, annual fee vs waiver, और category fit optimize करें। APR कम matter करता है अगर आप कभी revolve नहीं करते।

अगर कभी-कभी balance carry करते हैं (revolver): interest rate (APR) और minimum due behaviour ज़्यादा matter करते हैं reward points से।

Step 3 — Card 'Superpowers' को अपने Top Buckets से Match करें

अपने top buckets जानने के बाद, archetypes shortlist करें:

- Heavy online, many merchants: flat online cashback — e.g. CASHBACK SBI Card (हमारे data में 5% online)

- Amazon specific: Amazon Pay ICICI (₹0 fee, 5% Prime)

- Fuel + utility: Google Pay bills पर Axis ACE (5%)

- Dining + lifestyle: SBI SimplyCLICK

- Travel + forex: zero-forex cards जैसे Scapia

Step 4 — Filter करें कि Bank actually approve करेगा

Published minimum income और credit score floors बहुत अलग होते हैं। CardCheck पर हर card page पर eligibility fields issuer disclosures से आती हैं — card directory filters use करें।

Humble examples से: कुछ entry-level cards ₹15,000/महीना accept करते हैं; premium travel cards ₹50,000+ देखते हैं।

Step 5 — Annual Fee, Waiver Rules, और 'Break-Even' Spend Compare करें

₹500 fee card जो ₹40,000/महीना matched spend पर 4–5% earn करे, ₹0 fee card से बेहतर हो सकता है जो 0.5–1% earn करे। Rough maths:

- Extra annual earn ≈ (monthly matched spend × 12 × reward-rate difference)

- Minus joining + annual fee (और GST)

- Plus fee waiver savings अगर आप threshold hit कर सकते हैं

Step 6 — Apply से पहले Caps और Exclusions पढ़ें

Indian issuers routinely monthly या per-statement rewards cap करते हैं और rent, wallet loads, fuel, government, EMI exclude करते हैं। Same '5% online' headline वाले दो cards में ₹2,000 vs ₹5,000 monthly caps का फर्क हो सकता है।

CardCheck card pages पर Key Benefits section में exclusions listed हैं।

Step 7 — अपने numbers model करें (कोई एक blog table trust न करें)

दो-तीन finalists होने पर:

- Rewards Calculator में actual monthly spends enter करें

- Compare खोलें और finalists को fee, forex, lounge, और published earn पर side by side देखें

- किसी भी card पर apply करने से पहले issuer के MITC में details confirm करें

Step 8 — Sensible order में Apply करें और Card सही use करें

एक strong primary card plus optionally एक specialist (e.g. Amazon + utilities) ज़्यादातर लोगों के लिए काफी है। छह cards stack करने से missed due dates और fee leakage बढ़ता है।

RBI credit card FAQs से याद रखने वाली बातें:

- आप full outstanding बिना penalty के कभी भी pay कर सकते हैं

- Banks को charges clearly disclose करने होते हैं

FAQ

- क्या मुझे अपने salary bank का card लेना चाहिए?

केवल तभी अगर वह comparison में जीते। Same-bank cards से faster approval मिल सकता है, लेकिन cross-bank products अक्सर category rates या forex पर जीतते हैं।

- क्या lifetime-free card हमेशा best है?

नहीं अगर आपका spend high-accelerator categories में है। Fee waiver के साथ paid card या higher earn rate वाला card, 0% fee / 0.5–1% earn card से ज़्यादा rupees return कर सकता है।

- Calculator कितना accurate है?

यह database से published benefit lines, caps, और fee waiver rules model करता है। Real life merchant category codes और bank promotions पर depend करती है। Apply करने से पहले MITC में details confirm करें।

- मुझे decline हो गया। आगे क्या करूं?

3–6 महीने रुकें, existing lines पर utilisation कम करें, bureau errors correct करें, और IDFC FIRST WOW! जैसा secured card consider करें।