Picking a credit card from a brochure or a “pre-approved” SMS is fast. Picking one that matches how you actually spend takes a short, structured pass — and usually pays for itself in the first year.

This guide walks through eight practical steps: quantify your spend, decide how you will use credit, match categories (online, dining, fuel, travel, forex), check fees and caps, then model outcomes with tools. It aligns with what regulators expect you to watch (charges, consent, statements) and with how CardCheck surfaces issuer-published fees, rates, and benefit lines — not marketing adjectives.

Cards in this comparison

Compare now

Step 1 — Write down where your money actually goes

Open the last two or three full months of spends (bank statement, credit card statement, or UPI history). Bucket them roughly:

- Online retail (Amazon, Flipkart, brand sites)

- Food delivery and dining

- Groceries and supermarkets

- Fuel

- Bills and utilities (electricity, broadband, insurance premiums)

- Travel (flights, hotels, cabs)

- International / forex (foreign currency, overseas websites)

- Everything else

You do not need accounting precision — ±10% is enough to see which two or three buckets dominate. Cards are priced around category accelerators; if you skip this step, you optimising for the wrong headline rate.

Step 2 — Be honest: will you pay the full statement every month?

If yes (transactor): optimise for earn rate, annual fee vs waiver, and category fit. APR matters less if you never revolve.

If you sometimes carry a balance (revolver): the interest rate (APR) and minimum due behaviour matter more than reward points. RBI’s public FAQs on credit card conduct remind cardholders that if the total amount due is not cleared by the due date, interest-free credit is lost and interest may run from transaction dates on the outstanding amount — not only on “new” spend. In that situation, a lower APR or a smaller limit you can clear often beats a flashy cashback rate.

CardCheck lists APR bands and fees from issuer disclosures so you can compare total cost, not just rewards.

Step 3 — Match card “superpowers” to your top buckets

Once you know your top buckets, shortlist archetypes (you can compare concrete products on CardCheck):

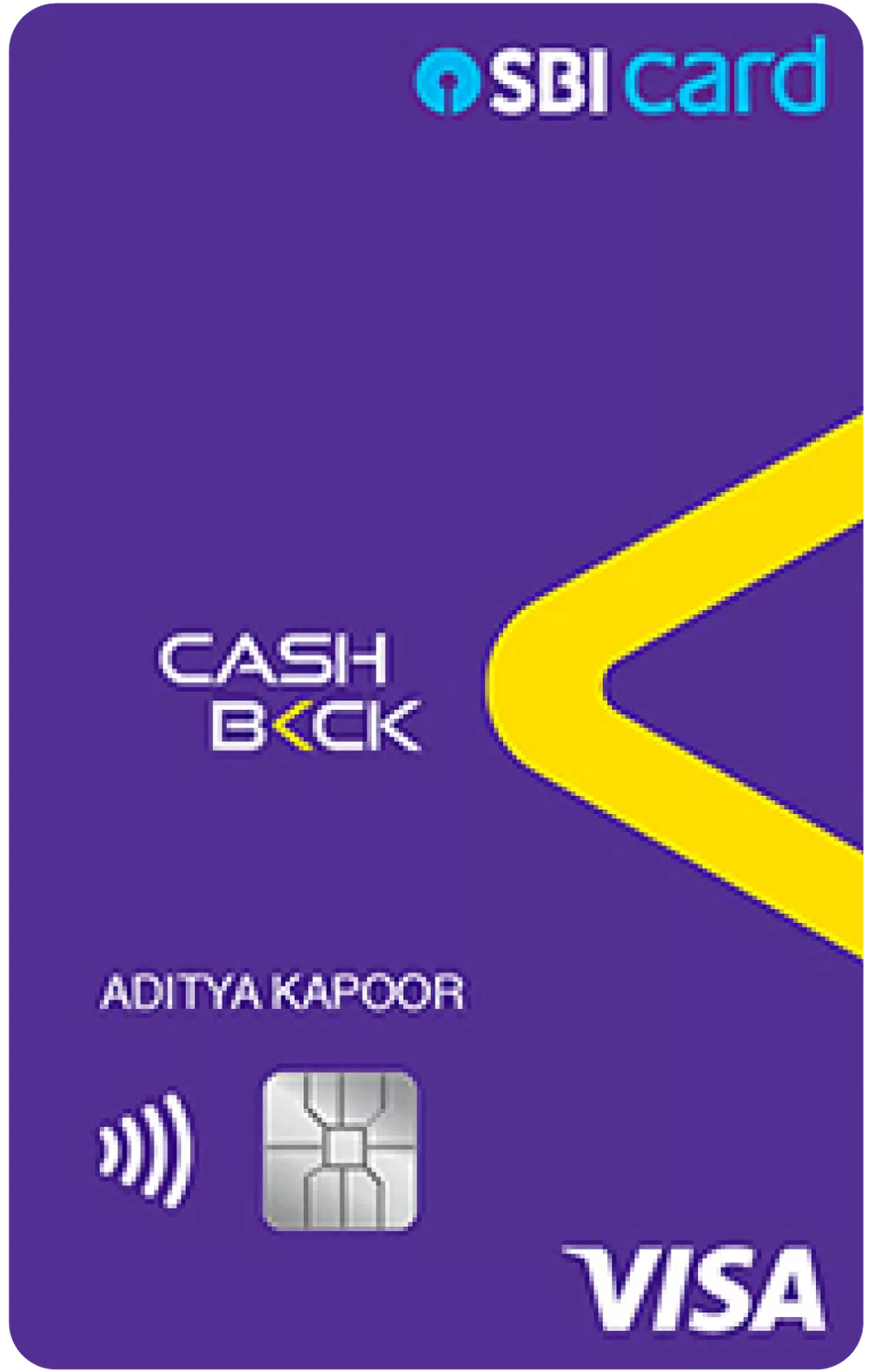

- Heavy online, many merchants: flat online cashback or broad e-commerce accelerators — e.g. CASHBACK SBI Card (5% online in our data) or category lists on HDFC Bank Millennia.

- Amazon-heavy, want zero fee: Amazon Pay ICICI Bank is lifetime free in our catalog with 5% back on Amazon.in for Prime members (3% non-Prime) — strong if that is your main storefront.

- Utilities, DTH, Google Pay bill pay: Axis Bank ACE shows 5% cashback on eligible utility and bill payments via Google Pay in our benefit lines (always confirm current app rules in the bank’s MITC).

- Dining + everyday retail at moderate fee: Amex SmartEarn™ targets Amazon and Swiggy at high earn rates in our data with a ₹495 fee band — good when those merchants are a large share.

- International trips or USD spends: look at forex markup (often 3.5% vs 2%) and lounge rules — e.g. HDFC Bank Diners Club Privilege lists 2% forex markup and Priority Pass visits in our database, alongside reward multipliers.

- Thin credit file or first card: secured products such as IDFC FIRST WOW! (fixed-deposit backed, 0% forex in our data) can build history while keeping costs predictable.

If your spend is evenly split with no dominant category, a flat-rate or simple multi-category card often beats juggling five niche products.

Step 4 — Filter by what the bank will actually approve

Published minimum income and credit score floors differ sharply. On CardCheck, eligibility fields on each card page come from issuer disclosures — use the card directory filters so you do not fall in love with a product you are unlikely to get.

Examples from our current data (always re-check the live page before applying): Axis Bank ACE lists ₹15,000/month minimum income; CASHBACK SBI Card lists ₹25,000/month; premium travel cards can list ₹1 lakh/month or more. Matching realistic eligibility saves hard pulls and disappointment.

Step 5 — Compare annual fee, waiver rules, and “break-even” spend

A ₹500 fee card that earns 4–5% on ₹40,000/month of matched spend can still beat a ₹0 fee card that earns 0.5–1% on the same pattern. Do the rough maths:

- Extra annual earn ≈ (monthly matched spend × 12 × reward-rate difference).

- Minus joining + annual fee (and GST), adjusted for fee waiver if you reliably hit the waiver threshold.

Waiver thresholds matter: a card waived at ₹1 lakh/year suits different users than one waived at ₹3 lakh/year. CardCheck surfaces these numbers on each card’s page from MITC-sourced fields.

Step 6 — Read caps and exclusions before you apply

Indian issuers routinely cap monthly or per-statement rewards and exclude rent, wallet loads, fuel, government, EMI, etc. Two cards with the same “5% online” headline can differ by ₹2,000 vs ₹5,000 monthly caps — that changes who “wins” for heavy spenders.

Use the Key benefits and exclusions sections on CardCheck (sourced from issuer materials). If a benefit line is missing, assume you cannot rely on it until you confirm on the bank’s PDF or app.

Step 7 — Model your own numbers (do not trust a single blog table)

Once you have two or three finalists:

- Enter your actual monthly spends in the Rewards Calculator — it uses the same category and cap logic as our editorial rankings.

- Open Compare and put finalists side by side on fee, forex, lounge, and published rates.

This catches cases where a lower headline rate with no cap beats a higher rate that maxes out mid-month.

Step 8 — Apply in a sensible order and use the card properly

One strong primary card plus optionally one specialist (e.g. Amazon + utilities) is enough for most people. Stacking six cards early increases missed due dates and fee leakage.

Regulator-side basics worth remembering (from RBI’s credit card FAQs): issuers must not issue unsolicited cards without consent; if you receive one, do not activate it and follow the bank’s closure process. For disputes, escalate through the bank first, then the RBI Integrated Ombudsman if needed (cms.rbi.org.in).

Bottom line: the “right” card is the one whose published earn structure, fee/waiver, and exclusions fit your spend pattern — verified with a calculator, not a hoarding instinct.

FAQ

- Should I get the same bank’s card as my salary account?

Only if it wins the comparison. Same-bank cards can mean faster approval or pre-approved limits, but cross-bank products often win on category rates or forex. Run the Rewards Calculator with your spends before defaulting to the salary bank.

- Is a lifetime-free card always better?

Not if your spend is large in high-accelerator categories. A paid card with a fee waiver you can hit, or a higher earn rate net of fee, can return more rupees per year than a 0% fee / 0.5–1% earn card. Compare net rupees after fee, not fee alone.

- How accurate is CardCheck’s calculator?

It models published benefit lines, caps, and fee waiver rules from our database. Real life depends on merchant category codes, bank promotions, and rule changes. Treat output as a strong estimate, then confirm details in the issuer’s MITC before applying.

- I was declined. What next?

Wait 3–6 months, reduce utilisation on existing lines, correct bureau errors, and consider a secured card such as IDFC FIRST WOW! to build a clean payment history. Avoid rapid multiple applications in the same month.