A decline stings, especially when the message is vague. In India, regulated card-issuers follow Reserve Bank of India rules on what they must tell you when they say no. Separately, your credit report (often CIBIL / Experian / Equifax / CRIF High Mark) is usually part of the story — but income, internal limits, and application quality matter too.

This article lists typical reasons aligned with what banks look at — not a prediction for your next application. For the exact rule on communicating rejection, see the RBI Master Direction link below.

Cards in this comparison

Compare now

What RBI requires when an application is rejected

Under the Reserve Bank’s Master Direction on credit & debit card issuance and conduct, card-issuers are directed that if a credit card application is rejected, they shall convey in writing the specific reason(s) that led to the rejection. The full legal text is on RBI’s site (download the PDF from that notification page).

If you only got a generic SMS, keep a screenshot / email trail and ask the bank’s official channels for the written communication you are meant to receive under this framework.

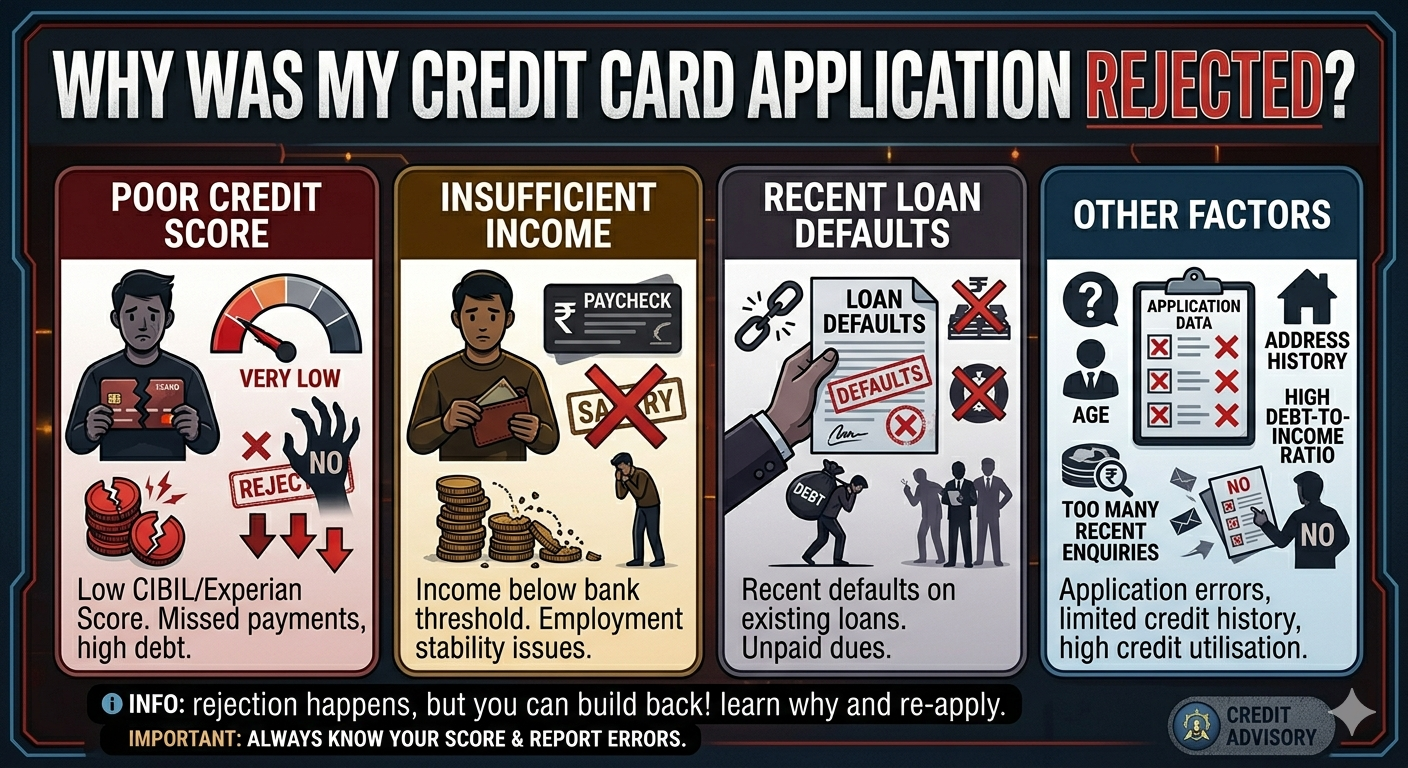

Weak bureau score or negative credit history

TransUnion CIBIL describes the score as a 3‑digit summary of credit history; published materials state scores range from 300 to 900 — see CIBIL’s consumer article. Missed EMIs, defaults, or high balances on the report usually hurt approval odds for unsecured cards.

India has four credit bureaus; the bank may pull one or more. Report errors can happen — bureaus run dispute processes on their websites; fixing a genuine mistake can change outcomes on re-application.

Income or job does not match the card’s policy

Cards are unsecured. Issuers set minimum income bands, employer / vintage checks, and internal debt-to-income tests. A salary below the product’s published or internal bar, unstable employment, or undisclosed existing EMIs can trigger a no even when the score is decent.

Recent serious delinquency or “settled” accounts

Recent loan or card defaults, write-offs, or settled-for-less entries flag higher risk. Some products have cooling-off expectations; the same bank may still see old dues on its own systems even if the bureau later updates.

Other frequent factors (application + behaviour)

- Too many hard enquiries in a short window — each new loan / card application can add an enquiry line.

- Very high credit utilisation on existing cards (using most of the limit every month) — can read as stress even if you pay on time.

- Thin or new-to-credit file — little history means less data for the model; secured / FD-backed cards are a common first step on issuer sites.

- Age / residency outside the product’s eligibility published on the site.

- KYC mismatch — address / name / PAN issues vs proofs submitted.

These are examples, not a checklist your bank must match word-for-word.

What to do next

- Read the issuer’s decline letter / email and match it to your CIBIL (or other) report.

- Dispute wrong bureau data on the bureau portal with evidence.

- Reduce new applications for a few months; pay down revolving balances.

- If the bank does not give a clear written reason after you ask on recorded channels, use the complaint / nodal route, then review RBI’s credit-card consumer FAQ — link — for escalation options (e.g. Integrated Ombudsman after timelines).

Compare cards on CardCheck when you are ready to re-apply with fees and rewards in view — still read the issuer’s latest eligibility page.

Disclaimer

Education only — not legal advice. The written-reason requirement is paraphrased from the RBI Master Direction; read the official PDF for exact wording. Approval remains solely with the issuer.

FAQ

- Does the bank have to tell me the exact reason in writing?

The RBI Master Direction states that on rejection of a credit card application, the card-issuer shall convey in writing the specific reason(s) — see the notification and its PDF. If you did not receive this, escalate on the bank’s ticketed channel and keep copies.

- Is CIBIL the only score that matters?

No. Lenders may use CIBIL, Experian, Equifax, or CRIF High Mark (or more than one). CIBIL publishes a 300–900 scale in its consumer materials (article) — that is the bureau model, not the bank’s internal cut-off.

- Will one more application hurt my score?

Each new application can add a hard enquiry line on the report. Several in a short period often worsens short-term approval odds. Space out applications after a decline.