A ₹45,000 phone swipe feels fine until the statement lands. You stare at the total, wonder if you should pay in full, and then spot Convert to EMI in your bank app — instant relief dressed as a button.

That button is real utility. It can stop you from revolving at 40%-plus annual interest on the unpaid chunk. It can also quietly add processing fees, GST on interest, limit blocks, and reward exclusions you only notice after the first instalment clears.

This guide is a bank-by-bank breakdown of post-purchase EMI conversion on Indian credit cards — HDFC SmartEMI, ICICI EMI on Call, SBI Flexipay, Axis, Kotak, Amex Plan It, OneCard, and more. Rates here are indicative ranges from issuer tariff pages; your app shows the binding offer before you confirm.

RBI expects issuers to spell out card charges clearly — skim credit card FAQs for consumers once so marketing copy and your statement speak the same language.

Cards in this comparison

Compare now

HDFC Bank EasyEMI Credit Card

Annual fee: ₹500

HDFC Millennia Credit Card

Annual fee: ₹1,000

Amazon Pay ICICI Bank Credit Card

Annual fee: ₹0

SimplyCLICK SBI Card

Annual fee: ₹499

Flipkart Axis Bank Credit Card

Annual fee: ₹500

OneCard Metal Credit Card

Annual fee: ₹0

American Express Membership Rewards Credit Card

Annual fee: ₹4,500

What credit card EMI conversion actually does

EMI conversion turns an eligible single purchase or statement slice into fixed monthly instalments. Each instalment carries principal plus finance charges at a rate the issuer quotes at conversion time — not the headline no-cost EMI rate you see at checkout on Amazon or Flipkart.

Three lanes matter for Indian shoppers:

- Checkout no-cost EMI — merchant or brand subsidy at the point of sale (covered in depth in our no-cost EMI explainer).

- Post-purchase conversion — you already swiped; the bank lets you restructure via app, net banking, or phone (this article’s focus).

- EMI-first cards — products built around instalment purchases (HDFC Easy EMI is the clearest example in our catalogue).

Catch most people miss: converting does not erase the purchase from your life. Many banks block the full ticket on your credit limit until principal amortises. Reward programmes often exclude EMI conversions from cashback or points — so the “convenience” can cost perks too.

Bank-by-bank EMI conversion comparison (2026 snapshot)

Every bank names the product differently, but the mechanics rhyme. Compare total rupee outflow (interest + fees + GST), not just the monthly EMI figure.

| Bank | Programme | Indicative interest | Processing fee | Typical tenures | Foreclosure (indicative) |

|---|---|---|---|---|---|

| HDFC Bank | SmartEMI | 12–18% p.a. | ₹99–₹749 + GST | 3–24 months | ~3% of outstanding |

| ICICI Bank | EMI on Call | 12–18% p.a. | 1–2% or flat ₹199–₹499 + GST | 3–24 months | ~3% of outstanding |

| SBI Card | Flexipay | 13–24% p.a. | 1–2% or flat ₹99–₹500 + GST | 3–24 months | ~3% of outstanding |

| Axis Bank | Convert to EMI | 12–24% p.a. | ₹199–₹699 + GST | 3–48 months | 2–3% of outstanding |

| Kotak Mahindra Bank | Transaction to EMI | 15–22% p.a. | Up to 3.5% of amount | 3–48 months | ~2% of outstanding |

| American Express | Plan It | ~12–21% p.a. | Often low or nil | Flexible plans | Varies by plan |

| OneCard | In-app EMI | ~12–18% p.a. | Often marketed as ₹0 | 3–24 months | Check app before confirming |

How to read this table: numbers shift by card tier, CIBIL band, and promotional windows. The sanction screen in your app is the contract — screenshot it before you tap confirm.

HDFC Bank — SmartEMI and the Easy EMI card

HDFC’s SmartEMI is the reference point many shoppers know. You can convert recent retail transactions or outstanding statement balances through the HDFC app or net banking, usually above a minimum ticket (often ₹2,500+ for purchases — verify live).

Typical SmartEMI traits:

- Interest band: roughly 12–18% p.a. on reducing balance for standard conversions.

- Processing fee: commonly ₹99–₹749 plus GST, depending on tenure and channel.

- Foreclosure: expect a percentage of outstanding principal if you close early — not automatically free.

- Limit block: full purchase amount may sit on your limit until principal frees up month by month.

HDFC Bank Easy EMI Credit Card

Who it suits: HDFC customers who plan electronics, appliances, or travel on EMI and can route spends through SmartBuy.

EMI angle: purpose-built for instalment buyers — 5% cashback on SmartBuy EMI in eligible categories plus 1% on other spends in product summaries. Annual fee waiver sits around ₹50,000 annual spend in catalogue data.

Catch: the boosted cashback is tied to SmartBuy EMI, not every random EMI you convert later.

HDFC Bank Millennia Credit Card

Who it suits: generalist HDFC users who want 5% partner cashback and may occasionally use SmartEMI on big tickets.

EMI angle: SmartEMI works on Millennia like any HDFC Visa/Mastercard — but partner cashback exclusions often apply to EMI-tagged spends. Model net benefit before assuming rewards stack.

ICICI Bank — EMI on Call

ICICI brands post-purchase conversion as EMI on Call. Eligible retail transactions (and sometimes statement balances) can move to instalments via iMobile, InstaBIZ, or customer care.

Typical traits:

- Interest: often quoted around 12–18% p.a. — premium cards may see sharper promotional slabs.

- Processing fee: percentage of principal (1–2%) or a flat ₹199–₹499 line plus GST, depending on channel.

- Tenures: commonly 3, 6, 9, 12, 18, 24 months.

- Rewards: EMI conversions usually sit in exclusion lists for Amazon and other partner accelerators.

Amazon Pay ICICI Bank Credit Card

Who it suits: heavy Amazon shoppers who may occasionally EMI a phone or appliance.

EMI angle: EMI on Call is available on this card like other ICICI Visa products. Amazon accelerator cashback may not apply on EMI-tagged spends — compare upfront payment vs EMI total before checkout.

Practical tip: if Amazon shows no-cost EMI at checkout, that is a different rail from EMI on Call on an already-swipe transaction. Read the confirmation screen separately for each.

SBI Card — Flexipay

SBI Card’s Flexipay converts outstanding retail balances or selected transactions into EMIs. Access via SBI Card app, YONO, or helpline.

Typical traits:

- Interest: broadly 13–24% p.a. depending on card and risk band — upper band hurts on longer tenures.

- Processing fee: 1–2% of amount or flat fee capped around ₹500, plus GST.

- Minimum ticket: often ₹2,500+ for transaction-level conversion (confirm live).

- Missed EMI: can trigger penal charges and push remaining balance back toward revolving card rates — read Flexipay T&C before opting in.

SimplyCLICK SBI Card

Who it suits: online-first users on Amazon, Flipkart, BookMyShow partner categories who sometimes need Flexipay breathing room.

EMI angle: Flexipay works, but partner reward points may not credit on EMI conversions. A ₹40,000 laptop on Flexipay can cost more in foregone points than the interest line suggests.

Axis Bank — Convert to EMI

Axis offers Convert to EMI on recent purchases and outstanding balances through Axis Mobile or internet banking. Tenures stretch up to 48 months on some conversions — longer tenure lowers EMI but raises total interest.

Typical traits:

- Interest: roughly 12–24% p.a. on reducing balance.

- Processing fee: commonly ₹199–₹699 plus GST.

- Foreclosure: 2–3% of outstanding principal is a common slab — verify on the offer letter.

- Exclusions: gold, cash advances, and some MCC categories may not convert.

Flipkart Axis Bank Credit Card

Who it suits: Flipkart-first shoppers who may stack accelerated cashback on everyday carts and use EMI on big sales.

EMI angle: post-purchase Convert to EMI is separate from Flipkart checkout EMI. Partner cashback rules may treat EMI spends differently — run the same SKU through Rewards Calculator for upfront vs EMI scenarios.

Kotak, Amex, and OneCard — different UX, same homework

Kotak 811 #DreamDifferent Credit Card

Kotak’s Transaction to EMI allows conversions from ₹2,500+ on many retail spends (gold commonly excluded). Issuer pages quote 15–22% p.a. interest and a processing fee up to 3.5% of the conversion amount, plus 2% foreclosure on outstanding principal.

Who it suits: Kotak customers who want a lifetime-free entry card and occasional EMI smoothing — not the cheapest rate table in India, but app-native and straightforward.

American Express Membership Rewards Credit Card

Amex Plan It lets you split eligible charges into instalments with upfront fee/interest disclosure — often cleaner UX than legacy SMS flows. Indicative pricing lands around 12–21% p.a. equivalent depending on plan length.

Who it suits: Amex loyalists who value predictable instalment schedules and already hit monthly MR bonus thresholds.

OneCard Metal Credit Card

OneCard markets in-app EMI conversion with zero processing fee on many plans — still verify interest rate and foreclosure in-app before confirming. The metal, lifetime-free positioning attracts users who hate fee surprises.

Who it suits: app-native spenders who want EMI without calling customer care and can accept partner-bank underwriting quirks.

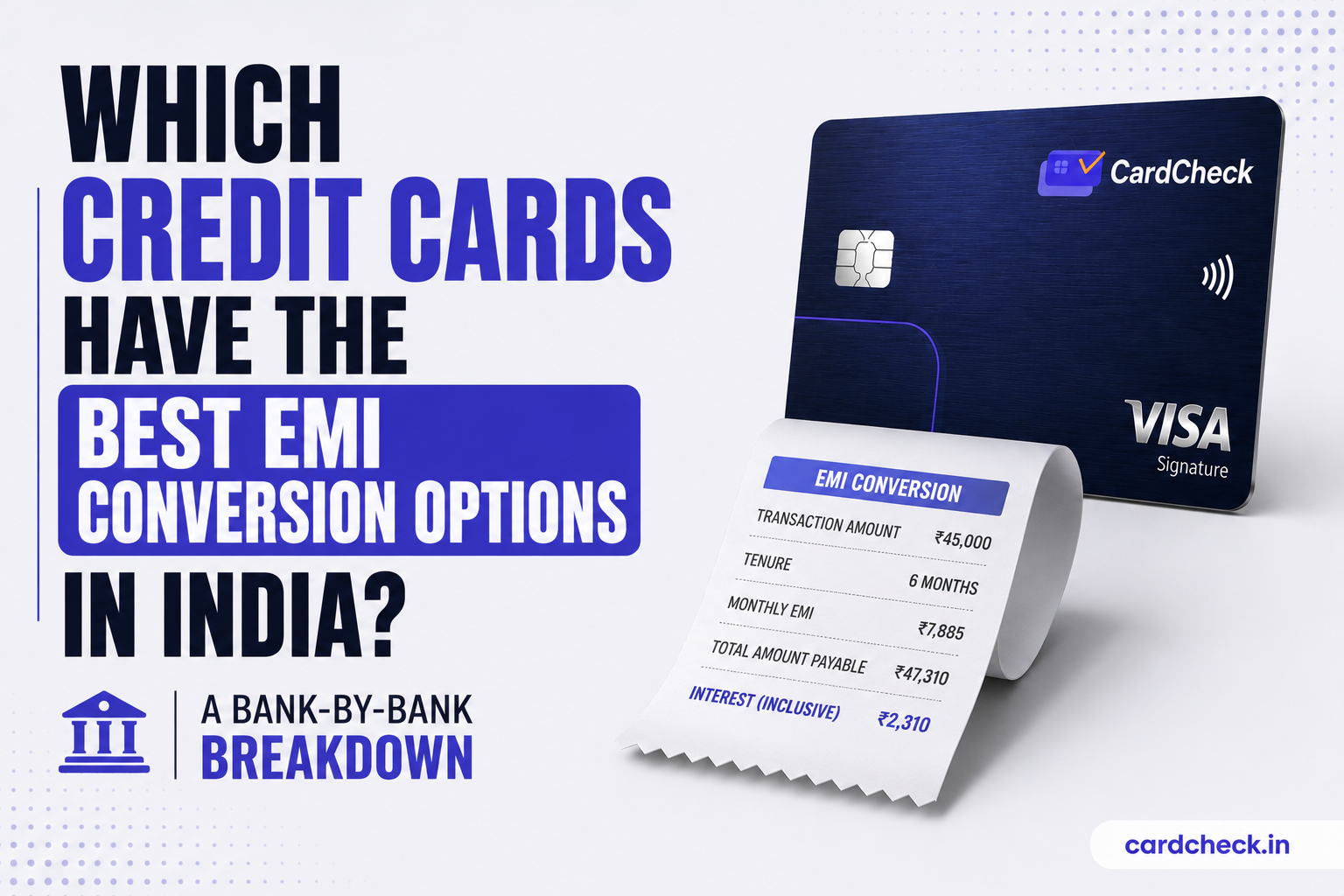

Worked example: ₹45,000 over 6 months

Suppose you convert a ₹45,000 retail purchase into a 6-month EMI at roughly 16% p.a. on reducing balance, with a ₹199 processing fee plus GST.

| Component | Amount (illustrative) |

|---|---|

| Transaction principal | ₹45,000 |

| Tenure | 6 months |

| Monthly EMI | ~₹7,885 |

| Total payable | ~₹47,310 |

| Interest component | ~₹2,310 |

| Processing fee (pre-GST) | ~₹199 |

That ₹2,310 “small” interest line is still real money — plus GST on interest and fees in most programmes. If the merchant offered 5% upfront cash discount (₹2,250 on ₹45,000), paying in full could beat conversion unless you genuinely need liquidity.

Always replicate with your bank’s sanction screen — rounding and rate bands move the total by hundreds of rupees.

When EMI conversion wins — and when a personal loan is cleaner

EMI conversion tends to work when:

- You would otherwise revolve part of the statement at 36–42% p.a. card rates.

- You need 3–12 months smoothing for a planned purchase and will not stack more EMIs on top of minimum-due habits.

- The issuer offer shows a clear amortisation schedule you can auto-debit.

A personal loan may beat card EMI when:

- Tenure runs beyond 12–18 months — PL rates near 10–18% p.a. can undercut card conversion on paper.

- You want one transparent APR without limit block side effects on future swipes.

- You are juggling multiple EMIs already — consolidation beats another card conversion layer.

Related: if minimum dues are the real problem, read minimum due trap before using EMI as a band-aid.

How to convert a purchase to EMI (step-by-step)

- Open your issuer app → Credit Cards → Convert to EMI / SmartEMI / Flexipay / Plan It (name varies).

- Pick the transaction or outstanding slice — confirm it is not gold, cash, or another excluded category.

- Read the sanction screen: principal, interest rate, tenure, processing fee, GST lines, foreclosure slab.

- Screenshot the offer — disputes are easier with timestamped proof.

- Check limit block after conversion — adjust travel or rent plans if available credit drops.

- Set payment autopay for the EMI due date — a missed slice can get expensive fast.

- Skip reward fantasies unless your MITC explicitly allows points on EMI — most do not.

If the app rate looks worse than a personal loan pre-approval, pause. Comparison shopping for 10 minutes can save thousands over the tenure.

Best EMI conversion picks by scenario

| Scenario | Practical lean | Why |

|---|---|---|

| Planned HDFC electronics on SmartBuy | HDFC Easy EMI | Cashback layered on EMI-eligible SmartBuy spends |

| Already hold HDFC Millennia | SmartEMI on Millennia | No new card — just verify reward exclusions |

| Amazon-heavy ICICI user | EMI on Call on Amazon Pay ICICI | Native issuer rail; compare vs checkout no-cost EMI |

| Flipkart-first shopper | Axis Convert to EMI on Flipkart Axis | Long tenures available — watch total interest |

| Fee-averse app user | OneCard in-app EMI | Zero processing fee positioning on many plans |

| Amex spender wanting clarity | Plan It on MRCC | Upfront instalment quote in familiar app UX |

Bottom line: the “best” EMI conversion is not a single card — it is the lowest total rupee outflow on your issuer offer for your tenure, without wrecking rewards you counted on or blocking limit you need next month.

Use CardCheck’s free Rewards Calculator to compare upfront vs EMI spend on your cards, then browse all cards side by side before the next big swipe.

FAQ

- Which Indian bank has the cheapest credit card EMI conversion?

There is no permanent winner — HDFC and ICICI often land in 12–18% p.a. bands for standard conversions, while SBI and Axis can quote higher on some cards.

OneCard frequently markets zero processing fee, and Amex Plan It can be competitive on fee disclosure.

Always compare the sanction screen total for your amount and tenure; a flat ₹200 fee difference matters less than a 3-point rate gap on ₹1 lakh.

- Can I convert an existing credit card purchase to EMI after swiping?

Yes — that is post-purchase conversion (SmartEMI, EMI on Call, Flexipay, etc.).

Eligibility windows vary: many issuers allow conversion within 30–90 days of the transaction and above a minimum ticket (often ₹2,500+).

Gold, cash advances, and some categories are commonly excluded.

- Is post-purchase EMI the same as no-cost EMI at checkout?

No.

Checkout no-cost EMI is a merchant/brand subsidised offer at payment time.

Post-purchase conversion uses the bank’s standard EMI tariff — interest and processing fees apply unless a separate promotion says otherwise.

See our no-cost EMI guide for checkout mechanics.

- Do I earn reward points when I convert a purchase to EMI?

Often no or reduced. Most issuers list EMI conversions in reward exclusion clauses alongside fuel, rent, wallets, and government spends.

Check your card’s reward terms before assuming cashback survives conversion.

- What happens to my credit limit when I convert to EMI?

Many banks block the full purchase amount on your limit, releasing it gradually as principal repays.

That can push up utilisation even while you pay on time — worth watching if you plan more swipes the same month.

- Can I foreclose a credit card EMI early?

Usually yes, but not always free. Foreclosure fees of 2–3% on outstanding principal are common, plus GST.

Run the math: if remaining interest is smaller than the foreclosure fee, riding out the tenure may be cheaper.

- What is the minimum amount to convert a credit card transaction to EMI?

Issuer-dependent — ₹2,500 is a frequent floor for retail purchases on HDFC, Kotak, and others.

Statement-balance conversions may use different thresholds.

Your app will grey out ineligible transactions.

Cards in this comparison

Compare nowHDFC Bank EasyEMI Credit Card

Annual fee: ₹500

HDFC Millennia Credit Card

Annual fee: ₹1,000

Amazon Pay ICICI Bank Credit Card

Annual fee: ₹0

SimplyCLICK SBI Card

Annual fee: ₹499

Flipkart Axis Bank Credit Card

Annual fee: ₹500

OneCard Metal Credit Card

Annual fee: ₹0

American Express Membership Rewards Credit Card

Annual fee: ₹4,500